.svg)

Powered by Keepgo

Powered by Keepgo

Published on:

July 2, 2026

Tags:

eSIM

Fintech

People like convenience: they don’t want to wait in queues to receive a service, to pick up an order, or to purchase a SIM or eSIM on arrival. Fintech has been developing its offering for years, and crypto wallets and neobanks offer more than tokens. They became diverse ecosystems, presenting everything from shopping mini apps to eSIM stores.

According to the latest figures from UN Tourism, around 306 million tourists traveled in Q1 this year, some of whom could be your existing customers and potential eSIM buyers. But even if they’re not, the demand keeps growing, and there’s no denying the trend. If you want to capitalize but lack the know-how on how to embed an eSIM solution in your fintech platform, this article has got you covered.

Modern users want to get significantly more out of the apps they use daily. They expect fintech companies to consistently and thoroughly meet their travel, payment, insurance, and connectivity needs.

WeChat has proven that embedded miniapps for various services are long-lasting and significantly impact the market. But if we look to the Southeast from China, Indonesia, through Grab and Gojek, is actively showing how popular fintech products have become. A mostly cash-based economy is rapidly digitizing, with even food stands having QR-payments tied to these super apps. They cover nearly everything: food delivery, taxis, massage services, banking, and much, much more.

A lot of popular fintech brands create their core customer base this way, and if you’re not expanding your offering, you’re leaving behind a service gap. If we take eSIMs, fintech platforms that have embedded them have a minimal 35% uplift in app transactions post-integration. In fact, even our partner cases at esimba.ai show it’s possible to earn $200,000+ in revenue selling eSIMs.

This popularity boom proves people actively want to stick with brands they like and seek a single all-in-one solution to eliminate digital clutter and multi-app setups. And this includes connectivity embedding.

Depending on your current needs and goals, there are three ways you can embed eSIM services into your ecosystem:

At our white-label eSIM platform, esimba.ai, we are proud to offer all three methods. We’ve described them in our blogs, and you can follow the links below to find out more.

If you’re not sure about how implementation could look, other brands could serve as an inspiration. Here is how fintech platforms offer connectivity to their clients.

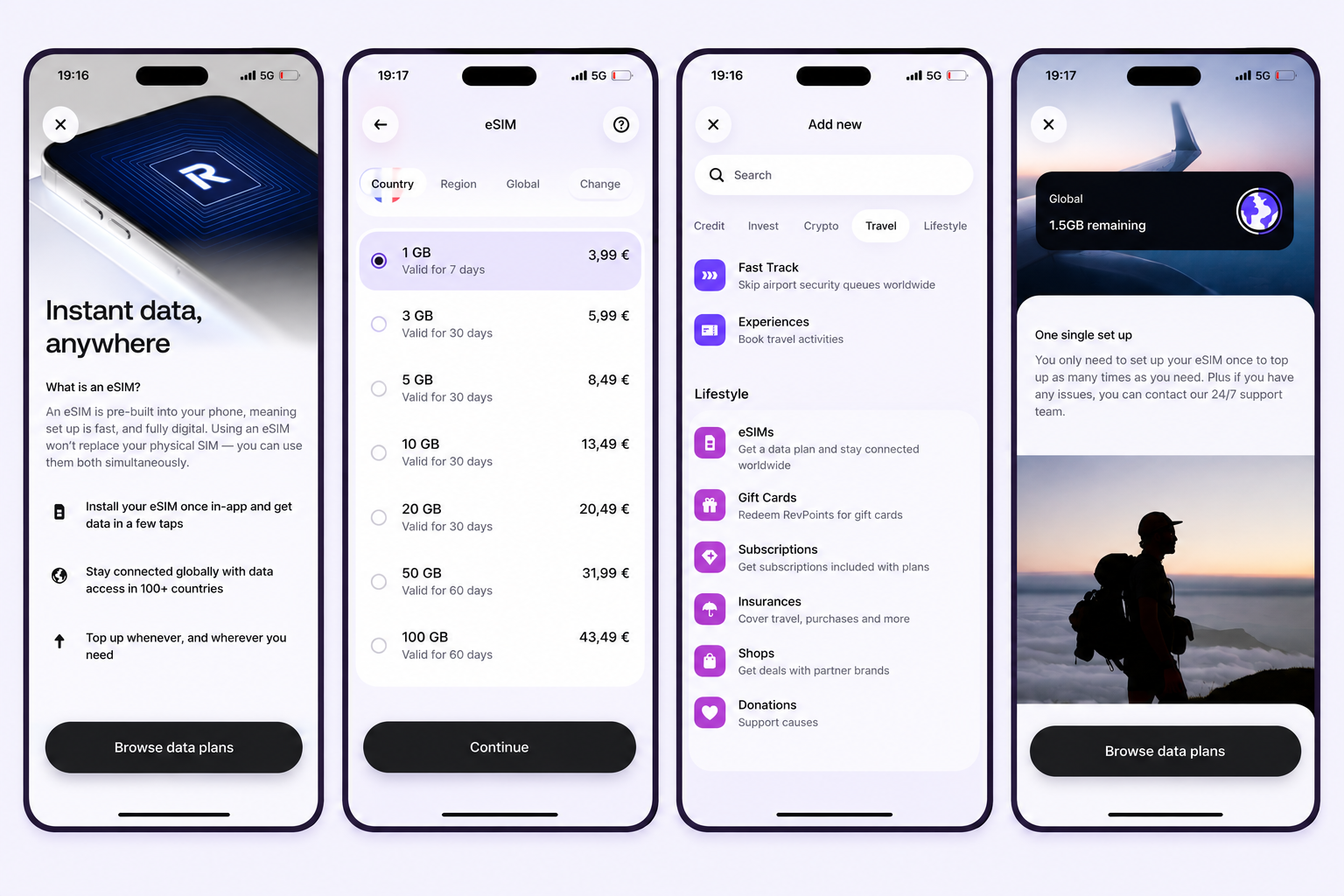

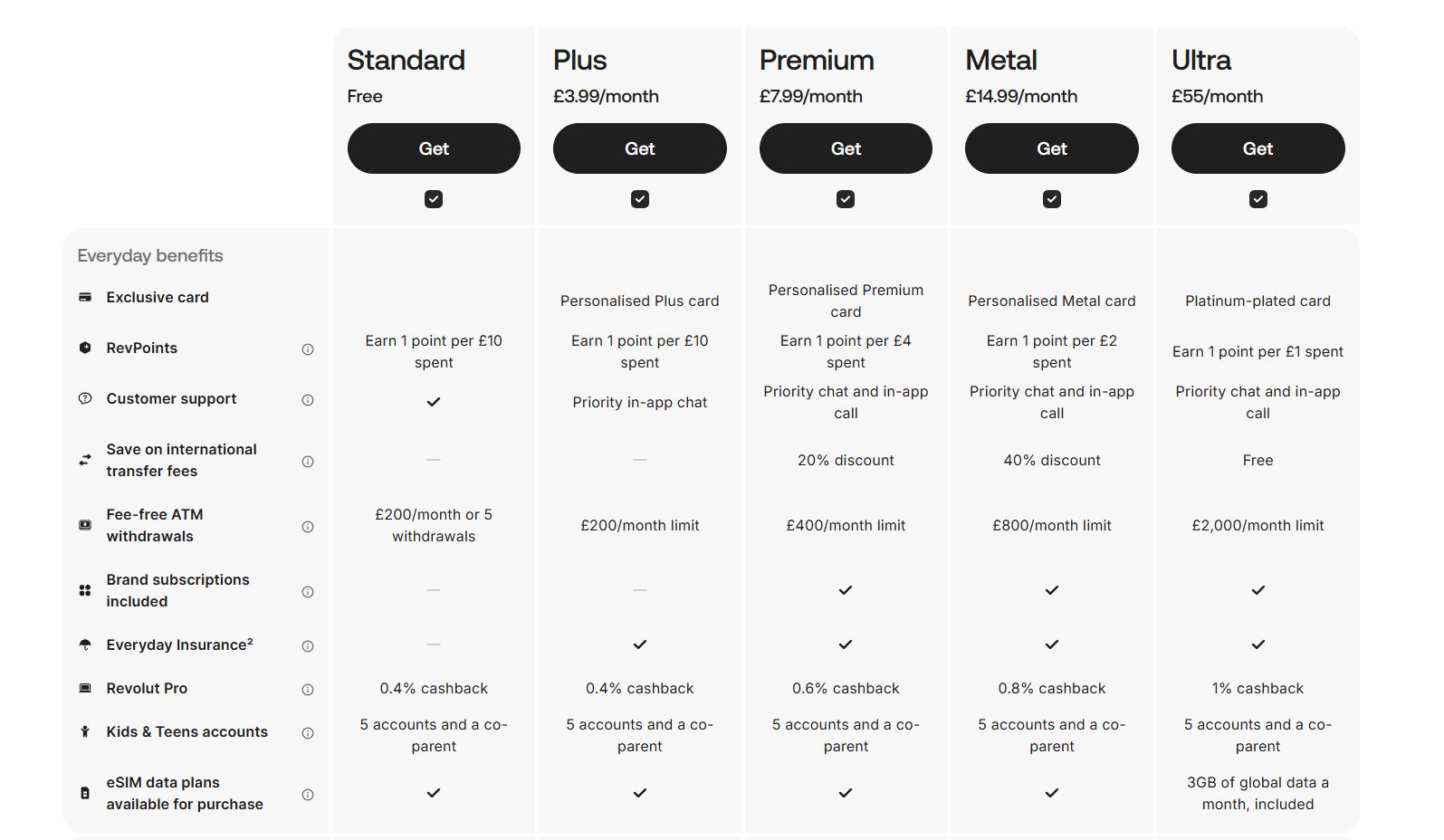

As with most fintech brands, Revolut found it needed to expand its offer. The neobank’s user base grew to 40+ million and span 150 countries. They wanted to find a way to add more value, and looked to an eSIM brand 1GLOBAL for a solution.

Using the operator’s API, they built connectivity into the app. In it, you can select “eSIMs” on the main page, which opens up a menu where you choose available data plans. You can sort by countries and even continents/ regions.

Right after the purchase, you can track active and expired eSIMs and even monitor usage. As their cardholders pay monthly subscriptions, the highest tier, Ultra, for €55, allows to get 3 GB of data for free.

Based on 1GLOBAL’s case study, 200,000 customers signed up for roaming data plans within a few weeks of launching. Introducing eSIMs has allowed to improve customer loyalty, creating an entirely new revenue channel for Revolut and benefiting the brand to this day.

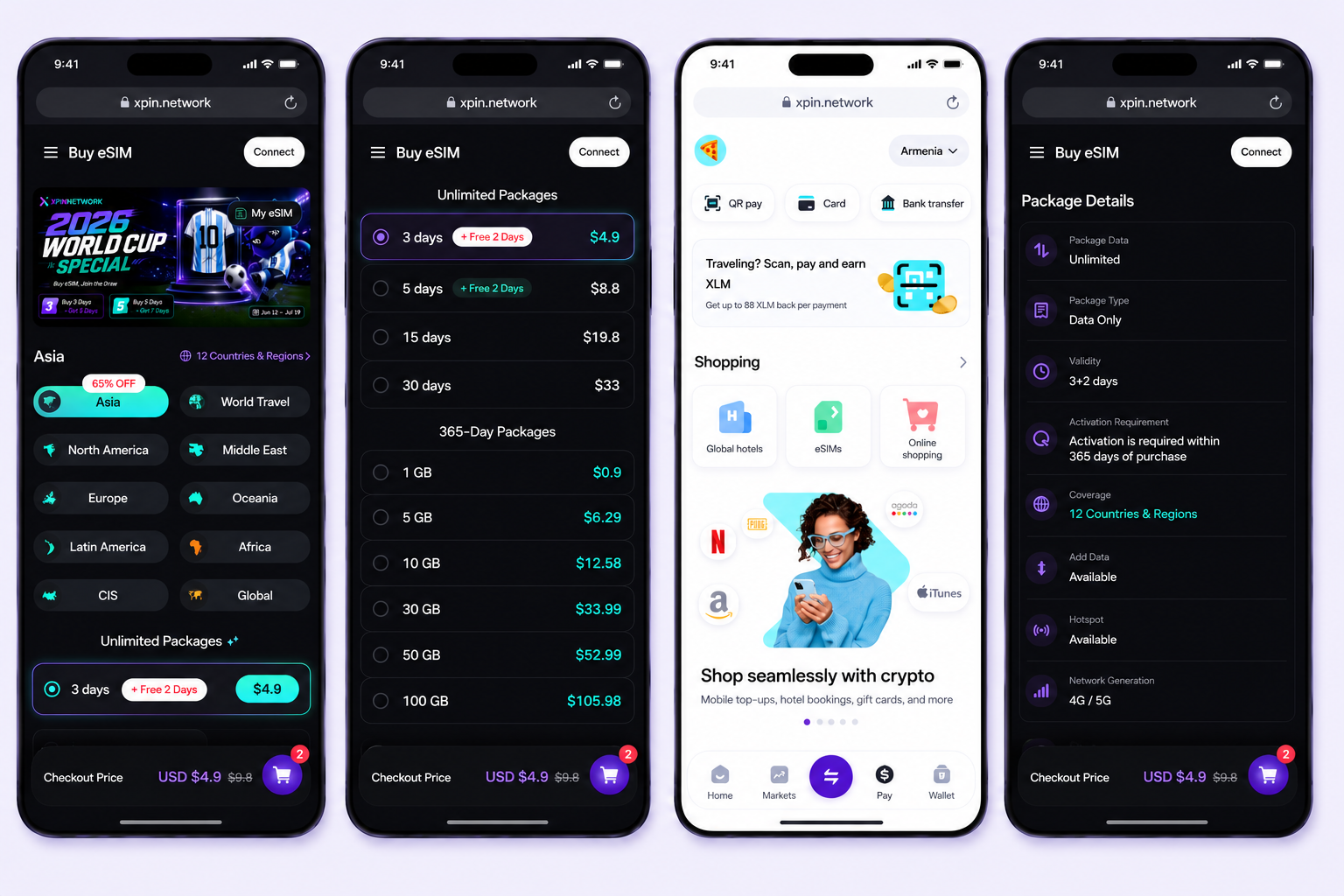

Bitget chose an interesting implementation pathway. They started with an eSIM store, accessible in the “Pay” section of the app. This was the result of partnering with XPin, which is a large decentralized network delivering connectivity through community-operated hardware. It uses AI-powered auto network switching to provide global coverage.

But the wallet also started supporting DePINSim ($ESIM), a decentralized connectivity protocol that positions itself as the world's first SIM that pays you. With these tokens, the idea is that users turn their phones into nodes on a decentralized network. Every byte of data consumed validates network coverage and earns $ESIM token rewards. In other words, eSIM data gains real monetary value, and users can use it by paying for more data, staking it, or trading it to BNB.

Although it’s difficult to glean profitability due to inherent crypto privacy, the integration shows how a Web3 wallet can layer eSIM connectivity on top of an existing financial product without it being the core business.

If, after carefully considering the above, you decide to partner up, there are a few important components to consider, starting with compliance.

When a fintech embeds eSIM through a white-label platform like esimba.ai, most of the technical compliance burden (GSMA SGP.22, provisioning infrastructure, telecom licensing) sits with the us, the provider. However, there’s a second layer that actually applies to you:

Monetization comes next. Here, you’ll find a plethora of options, all of which can be offered simultaneously if that fits the scope. Use these as idea fuel, not strict recommendations, aside from the more common implementation cases. You can offer eSIMs as:

If, after reading the article, you have a strong desire to partner with esimba.ai could help integrate connectivity into your model and easily allow you to scale. We offer coverage across 150+ countries, a fully managed model with pricing, provisioning, and customer support, and even a dedicated brand manager.

By partnering with us, you gain access to a premier network of carriers and start selling eSIMs in a matter of weeks. Our white-label apps take around 21 days, with API integration and a full webstore creation taking even less. We also offer zero-friction integrations with existing operators, and will soon offer eSIMs with real phone numbers.

eSIM in fintech is a competitive advantage, and the slower you move, the faster your competition will win over your customers. Reach out to us today to get there first and reap the rewards!

.svg)

As a global MVNO, esimba.ai, a subsidiary of Keepgo, provides you with the opportunity to offer your customers top-quality connectivity in 150+ countries.

.svg)